LEVATUS Perspective | The Quiet Transformation of Passive Investing

What the 2026 Initial Pubic Offering Wave Means for Index Exchange Traded Funds — and for You

Susan Dahl | CEO LEVATUS

Photo by Bill Jelen

A new wave of mega-IPOs could reshape public markets, with SpaceX, OpenAI, and Anthropic among the highest-valued private companies ever created. Their eventual listings will mark a new chapter for passive investing, as unprecedented amounts of market value enter major indexes and become incorporated into index-based investment strategies.

Yesterday, June 4, 2026, S&P Dow Jones Indices announced that it would not adopt any of the proposed changes to mega-cap eligibility rules for the S&P 500. After a month-long consultation, the index provider chose to maintain the existing 12-month seasoning period, the profitability requirement, and the 10% minimum public float threshold. This decision creates a clear and immediate divergence with Nasdaq, which implemented fast-entry rules effective May 1.

As a result, the three largest upcoming IPOs — SpaceX, OpenAI, and Anthropic — now face materially different paths to index inclusion depending on the benchmark they are measured against. The outcome resets expectations that had been forming around faster integration of trillion-dollar companies into the S&P 500 and underscores that not all major index providers are moving in the same direction on structural change. This also means that some of the largest passive Exchange Traded Funds will include substantially different holdings.

Executive Summary

Nasdaq-100 implemented fast-entry rules effective May 1, allowing qualifying new listings (top 40 by market cap, or market capitalization) to enter after just 15 trading days and removing the prior 10% minimum public float requirement.

S&P 500 rejected all proposed changes on June 4. The 12-month seasoning period, profitability requirement, and minimum 0.10 IWF rule remain fully in place.

SpaceX, OpenAI, and Anthropic therefore face materially different inclusion timelines: fast entry is now possible in the Nasdaq-100 (subject to size thresholds), while S&P 500 inclusion will still require the full 12 months of trading history plus demonstrated profitability.

The core investment implications around low-float mechanics, mechanical index buying pressure, elevated concentration, and the reduced reliability of historical index data remain relevant — particularly for Nasdaq-100 trackers.

The outcome is a meaningful development. It preserves the S&P 500's historical "quality filter" approach rather than creating size-based exceptions for the largest upcoming IPOs.

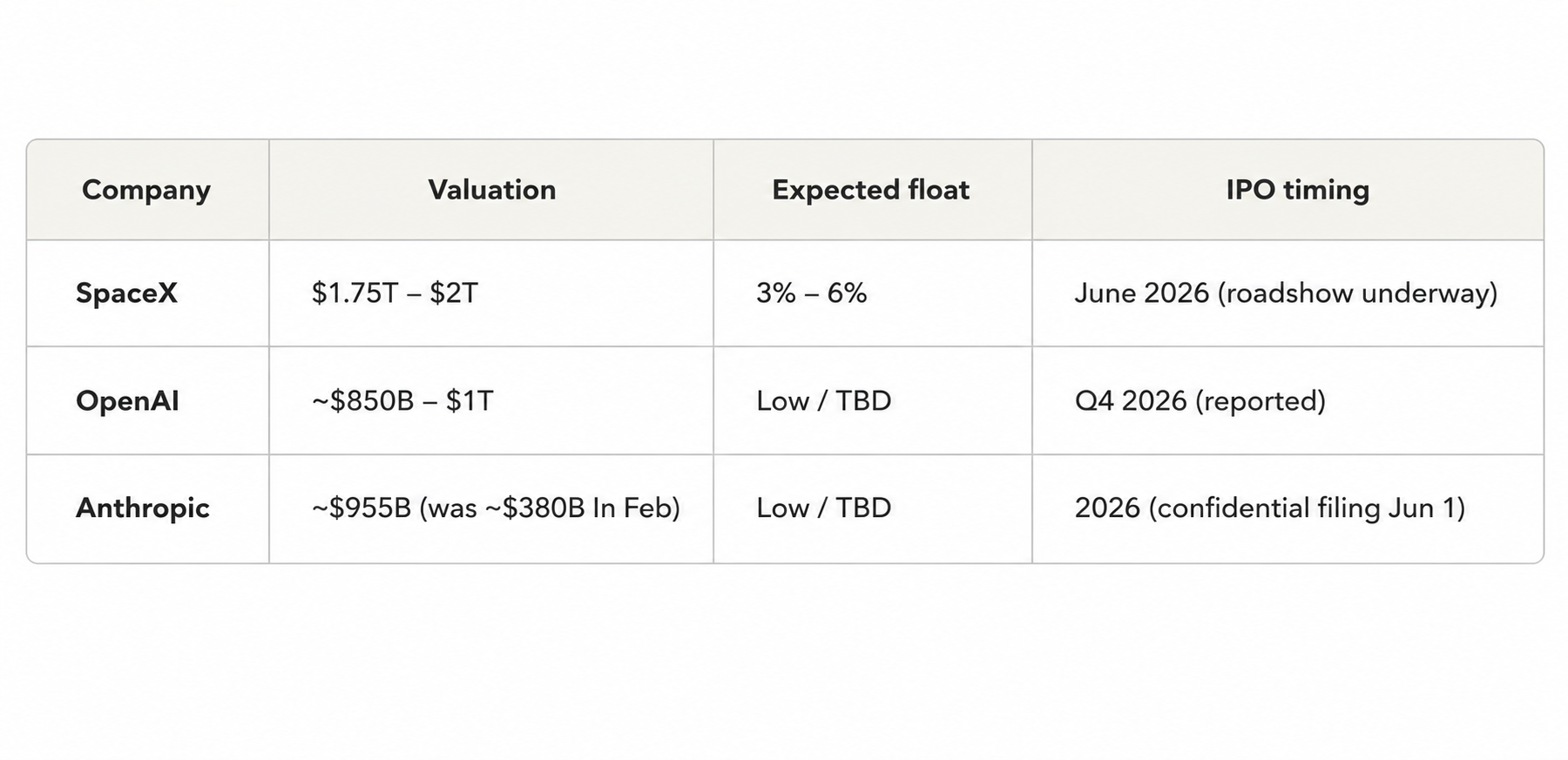

Three of the most valuable private companies in the world — SpaceX, OpenAI, and Anthropic — are preparing to go public. Combined, they represent an estimated $3 trillion+ in market value. That alone would make 2026 a historic year.

Another part of the story is equally interesting and important. It's what had to change — structurally, at the index level — to accommodate them. And what those changes mean for the investment vehicles that tens of millions of Americans have come to think of as simply 'the market.'

This note explains what's happening, what's confirmed, and what it means for how we think about index funds going forward.

“Passive investing is changing. Not in name. In structure.”

The Buffer Is Changing

For decades, there was a gap between when a company went public and when it entered a major index. The S&P 500 required twelve months of trading history — and four consecutive profitable quarters — before a company could even be considered for inclusion. The Nasdaq-100 had its own seasoning requirements, typically three months or more.

That gap served a purpose. It allowed price discovery. It kept IPO-day volatility away from the retirement accounts of people who never asked to be active traders.

However, the compression is no longer uniform. Nasdaq has moved decisively toward faster inclusion. The S&P 500 has chosen continuity.

Nasdaq Moves First

On March 30, Nasdaq announced a formal overhaul of its Nasdaq-100 methodology. The headline change: newly listed companies whose market capitalization ranks within the top 40 index constituents — currently a threshold around $100 billion — can join the index after just 15 trading days. The prior wait was at least three months; sometimes closer to a year.

Nasdaq also eliminated the 10% minimum public float requirement. This matters because all three major IPOs are expected to list with a very limited number of public shares — estimates place the initial float at somewhere between 3% and 8% of total shares outstanding. Under the old rules, they may not have qualified at all.

S&P Holds the Line

On April 30, S&P Dow Jones Indices opened a formal consultation on proposed changes to S&P 500 eligibility. The proposals were meaningful:

The seasoning period would be cut from twelve months to six for companies with a market cap at or above roughly $112 billion. More significantly, the profitability requirement — four consecutive quarters of positive GAAP (Generally Accepted Accounting Principles) earnings — could be waived entirely for companies that qualify as mega-caps. An exemption from the minimum 0.10 IWF was also proposed for mega-caps.

The consultation period closed May 28. On June 4, 2026, S&P Dow Jones Indices announced that no changes will be adopted. The existing eligibility criteria, including the 12-month seasoning period, financial viability/profitability screens, and minimum IWF of 0.10, remain in place for the S&P 500 and related indices. S&P determined that exceptions should not be granted solely based on market capitalization.

As a result, the anticipated fast-track path for mega-cap IPOs into the S&P 500 will not occur. SpaceX, OpenAI, and Anthropic will still need to meet the full traditional requirements for S&P 500 inclusion. This means that at its foundation, S&P index funds retain existing characteristics.

S&P did make one narrow accommodation: the S&P Total Market Index and related broad-market benchmarks received a new float exception, allowing companies whose public float exceeds the total market cap of the index's 100th largest constituent to bypass the standard 10% minimum float requirement. This ensures that total-market passive funds won't entirely miss historic listings — but it does nothing to accelerate entry into the S&P 500 itself.

“The S&P preserved core index principles by maintaining consistent application of key requirements, stating that exceptions should not be granted solely based on market capitalization.””

The Scale of What's Coming

The three anticipated IPOs are not simply large. They are large in a way that strains the mechanics of index construction. Their headline valuations alone would make 2026 extraordinary. Yet the much bigger and more lasting impact will not come from the initial capital raises or even the moment they enter major indices. It will come from what happens in the months that follow.

*Anthropic's ~$380B February 2026 funding round valuation has since been superseded by newer reports citing figures closer to $965B as of late May 2026.

Sources: Bloomberg, Reuters, company announcements, S&P Dow Jones Indices consultation documents.

SpaceX is launching its June 2026 IPO with only a ~4–5% public float, which produces very small initial weights in major indices. The S-1 (the formal registration statement companies file with the SEC — Securities and Exchange Commission — before going public) uses a staggered lock-up schedule that unlocks the large majority of non-Musk shares progressively, causing the tradable float (and therefore index weights) to expand significantly by November. Most indices are strictly float-adjusted, but the Nasdaq-100 applies modified weighting rules, allowing SpaceX's weight in QQQ (the principal ETF that tracks the Nasdaq-100) to ramp up materially and relatively quickly as the float grows over the first five to six months. By November, SpaceX's index weight could be roughly 8–10x higher than its initial post-IPO weight, as the float is expected to rise from ~4–5% to approximately 35–40% of total shares.

This is the critical distinction. In a conventional large IPO, the bulk of the public float is available from day one, and index inclusion (when it occurs) happens against a relatively stable share count. Here, the opposite is true. These companies are entering indices with only a sliver of their shares tradable, and that sliver will grow substantially over time through scheduled lock-up releases. As the investable float expands, float-adjusted indices will require passive and index-tracking funds to buy increasing quantities of shares simply to maintain their benchmark weights.

The result is not a single, contained capital event. It is a multi-month process of mechanical, rules-driven buying that intensifies as more shares become available. For the Nasdaq-100, the combination of fast-entry rules and modified low-float weighting accelerates this ramp. The cumulative capital that index funds will need to deploy over the first five to six months after SpaceX lists is likely to far exceed the capital raised in the IPO itself. The same dynamic could later apply to OpenAI and Anthropic if they adopt similarly low initial floats and phased unlock structures.

In short, the scale that matters most for passive investors and index construction is not the size of these companies on IPO day. It is the size of the ongoing, time-released adjustment that indices and the funds that track them will be forced to make as the float steadily expands.

Why Profitability Matters

The S&P 500 has historically functioned as something close to a quality filter. To earn inclusion, a company had to demonstrate that its business model worked — in the most basic sense of producing more revenue than it spent. Four consecutive quarters of positive GAAP earnings was the bar. That requirement kept the index anchored to companies with at least some fundamental grounding.

SpaceX disclosed a net loss of approximately $5 billion for full-year 2025 in its S-1 filing with the SEC — the formal registration statement companies file before going public. A significant portion of that loss stems from the February 2026 acquisition of xAI. OpenAI and Anthropic remain private and have not disclosed audited financials, but both are estimated to be losing several billion dollars annually, reflecting heavy ongoing investment in their respective businesses.

Under the rules S&P chose to preserve, none of the three would currently qualify for S&P 500 inclusion on profitability grounds alone — regardless of their size. That is precisely the point. The index was not designed to admit companies based on how large or consequential they are, but on whether they have demonstrated a working, profitable business model.

“The S&P 500’s profitability requirement isn’t just a technicality. It has historically served as a quality screen that distinguishes established operating businesses from earlier-stage companies still proving their economic model.”

What This Means for Index Valuation

When large companies are added to a market-cap-weighted index, the aggregate valuation statistics shift — not because existing companies became more expensive, but because the math of the index changes.

A Seeking Alpha market analysis in late April estimated that adding all three IPOs to the S&P 500 would raise the index's total market cap to approximately $60.3 trillion and give the new entrants a combined weight of roughly 5%. The earnings picture would soften, as the losses of the new members partially offset the profits of existing ones.

That concern has institutional backing. Bank of America Chief Investment Strategist Michael Hartnett has warned that the listings of SpaceX, OpenAI, and Anthropic could push the technology sector's weight in the S&P 500 past the 48% historical threshold — surpassing concentration peaks seen during the Roaring Twenties, the Nifty Fifty of the 1970s, and the dot-com era. The implication is not subtle: the index would be more concentrated in a single sector than at any point in modern market history.

Because the S&P proposals were not adopted, these specific effects on S&P 500 metrics will be delayed until the companies meet the full eligibility criteria. However, faster inclusion dynamics will apply in the Nasdaq-100 for any name that qualifies under the new fast-entry rules.

The precise numbers depend on final valuations, float sizes, and weighting methodology. What matters more than any specific figure is the directional reality: the valuation metrics you use to compare today's market against historical norms will be distorted by structural changes in what certain indices contain.

A P/E (price-to-earnings) ratio measured against a history that assumed the index was a collection of profitable companies becomes harder to interpret when that assumption no longer fully holds.

The Concentration Situation

Index concentration is not a new concern — but it is an intensifying one. At the peak of the dot-com bubble, the top ten holdings represented roughly 25% of the S&P 500. Today that figure is estimated between 30% and 40%, according to S&P Dow Jones Indices data and recent analysis from Goldman Sachs tracking Magnificent Seven concentration, reflecting the dominance of the companies sometimes called the Magnificent Seven.

The addition of trillion-dollar newcomers would push that concentration higher still — with an important wrinkle. Because the new entrants are expected to list with very low public float, index-tracking funds would be required to buy a large amount of shares from a very small available pool in the indices that admit them quickly. That mechanical demand, driven by index rules rather than investment judgment, has the potential to create pricing dynamics that are disconnected from fundamental value.

Academics and practitioners have flagged this. Owen Lamont of Acadian Asset Management described the 15-day inclusion window as simply too short for price discovery to occur. The concern is not abstract — it is about who absorbs the uncertainty that used to be absorbed by the seasoning period.

“Passive funds used to be the beneficiaries of price discovery. Under the new rules, they may become participants in it.”

A Note on Historical Analysis

When we model portfolio behavior — stress-testing allocations, projecting volatility, evaluating diversification — we rely on historical data about how indices have actually behaved. That analysis rests on certain assumptions about what the index was: a collection of seasoned, profitable companies, weighted by their genuine market presence.

If the structural rules change in some indices but not others, the historical record becomes a less reliable guide for those benchmarks that have changed. Not worthless — but less directly applicable. The beta (a measure of how much an investment moves relative to the broader market) of an index that contains actively price-discovering, low-float mega-caps is a different thing than the beta of the index we've been studying for decades.

Consider a straightforward illustration: a portfolio stress-tested against ten years of Nasdaq-100 historical volatility was calibrated against an index that required meaningful trading history and a minimum public float before admission. If that same index now admits a $2 trillion company after 15 trading days with a 4% float, the historical volatility data no longer fully describes the instrument. The stress test hasn't changed. The index has.

This isn't a reason to panic. It is a reason to be more deliberate — to understand what you own, what the benchmarks you're measured against actually contain, and how the rules governing them have changed (or stayed the same).

What We're Watching

The S&P consultation has concluded with no changes to eligibility rules. Attention now shifts to how the existing rules interact with these large, low-float IPOs in practice.

We'll be watching the float dynamics closely, especially in the Nasdaq-100. The difference between a 3% float and a 7% float for a $2 trillion company is hundreds of billions of dollars in the forced buying required from passive funds. The mechanics of inclusion will matter enormously for price behavior in the weeks after any fast-entry event.

SpaceX is expected to begin trading in mid-June. Any fast entry into the Nasdaq-100 (if size thresholds are met) would occur on an accelerated timeline relative to historical norms, while S&P 500 inclusion will still require the full 12-month seasoning plus demonstrated profitability.

In our own portfolio construction work, we are paying particular attention to the distinction between S&P 500 trackers and Nasdaq-100 trackers in client allocations — not because one is categorically superior, but because they are now operating under meaningfully different structural rules, and that difference deserves to be explicit rather than assumed.

None of this is a call to abandon index funds. They remain, for most purposes, a sensible and efficient approach to market participation. But 'passive' investing has never meant 'inert.' Indices are constructed by committees, governed by rules, and shaped by decisions — and those decisions are evolving in ways that matter, even when some proposed changes are ultimately not adopted.

At LEVATUS, we believe clarity is the foundation of living freely — and that includes being clear about what your investments actually are and how the rules governing them have changed, or in some cases, deliberately have not.

June 5, 2026

This note is for informational purposes only and does not constitute investment advice. All rule changes are described based on official announcements as of June 5, 2026. Please consult your advisor before making any investment decisions.

investment, Tax, estate

LEVATUS | Distilling complex topics down to their essence

ABOUT THE AUTHOR

Susan Dahl is a seasoned executive, industry leader, and dedicated client advisor, with over thirty years of international and domestic financial experience. Susan is known for her ability to unravel complex questions, and has a steadfast commitment to well designed process. This background has translated directly into her work on investment process design for private wealth clients, as well the industry leading LEVATUS Integrated Wealth Service model; a modern design that addresses the many ways financial decision making impacts - financial security, relationships, and sense of purpose across generations. A deep and diverse background that extends from global investing, to risk management, to process development and planning, has laid the groundwork for an advisory solution that asks more of wealth. Susan shares some her most recent work in this TEDx , Can Happy Make You Money?

ways to share

“Whatever it is, the way you tell your story online can make all the difference.”

A new wave of mega-IPOs could reshape public markets, with SpaceX, OpenAI, and Anthropic among the highest-valued private companies ever created. Their eventual listings will mark a new chapter for passive investing, as unprecedented amounts of market value enter major indexes and become incorporated into index-based investment strategies.